Wayne Gretzky has a great saying about why he was so successful as a hockey player.

The Great One said… “I skate to where the puck is going to be, not where it has been.”

Right now, you need to be skating to where the AI Trade is going to be, not where it’s been. This is because there is another group of stocks that are ready to cash in on the AI movement, and the “Crowd” has yet to zero in on these stocks.

That means that you can be early to a new trend in the AI Industry

Let’s start with a broad statement. The NVIDIA (NVDA), AMD (AMD) and other early “AI trades” will continue to make money for investors, but there’s a problem.

The companies I mentioned above are crowded trades. Everyone that wants to own NVIDIA likely owns it. The market has figured out their value, meaning that these stocks are now going to trade on multiples that are “set”.

NVIDIA can move the revenue and earnings needle higher, but they’re not going to see the same blockbuster success that they’ve seen since the AI trend started in 2020.

It’s time for them to hand the torch to the next group of stocks that will see parabolic growth as Artificial Intelligence goes from the development phase to application into our daily life.

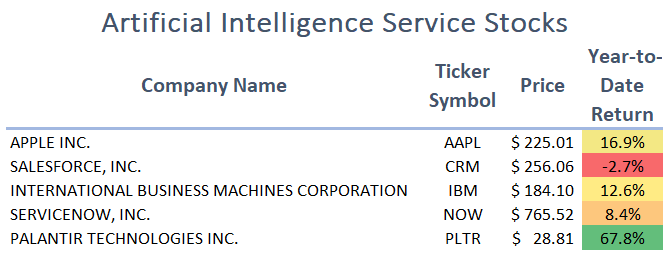

While there are many companies that will start to hit your radar in the “AI Services” industry, the following is a short list of the companies that are already aggressively growing revenue and earnings as their existing business lines adopt Artificial Intelligence.

These, among other AI Service stocks, are the next wave of investing. They’re the AI gatekeepers that will bring efficiency and productivity to companies that are looking for plug-and-play style products to enhance their offerings.

Computer programing, client management, consumer applications, government and health care applications, they’re all covered by these five AI Service companies.

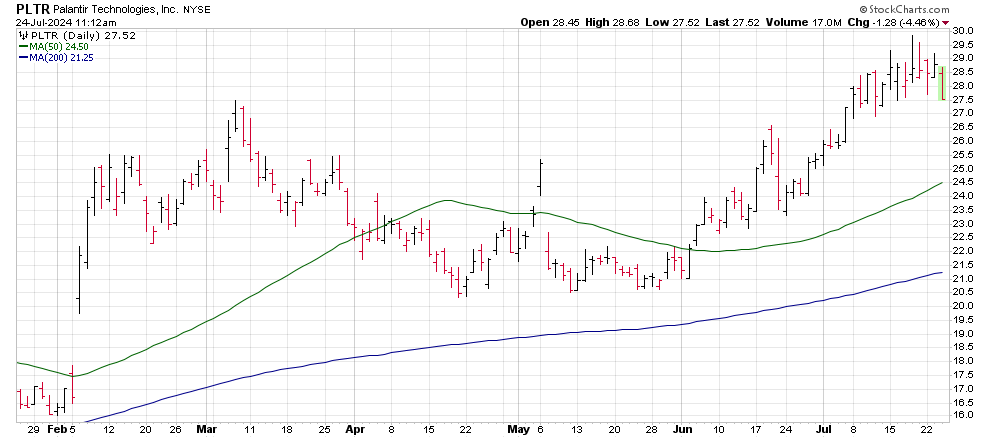

Last quarter, this group of companies saw a drop in their stock prices after their individual earnings, with the exception of Palantir.

Companies like IBM (IBM), Salesforce.com (CRM), and ServiceNow (NOW) all guided their earnings estimates slightly lower as the businesses that they are rolling new AI-enhanced products out to hit the “pause” button.

The reason? Companies have been concerned about a short slowdown in the economy. This resulted in delays to capital expenditures, namely for implementing new AI technologies. That pause only delays the inevitable.

Management for companies both large and small will begin to move forward with their AI spending plans as the Fed now indicating that interest rates are likely to start declining in September. This means that these AI Service companies are set to launch into a strong end of the year rally.

One AI Service Standout, Salesforce.com

Salesforce.com (CRM) has been implementing AI into their client products, allowing their customers to Sell Faster using their customer Data & AI.

Their products help to automate sales tasks, accelerate customer decisions, and guide sales forces with “Salesforce Sales Cloud”.

Salesforce.com shares dropped more than 30% last quarter after the company disclosed that several large clients had been slowing progress on signing new contracts with the company and this service. The delays caused Salesforce’s management to lower their earnings outlook for this quarter, but to also raise their guidance for the rest of their fiscal year.

This suggests that the company expects new business to pick up as we head into the end of 2024 and into 2025 as fears of a recession begin to drop.

The 30% decline in shares has provided an opportunity for investors that were looking for an opportunity to “buy the dip” on CRM stock to do so as the stock’s PE ratio of 44 puts it inline with other software providers.

Shares are down almost 3% for the year, meaning that investors will be looking to pick up this “value trade” at the first sign of strength.

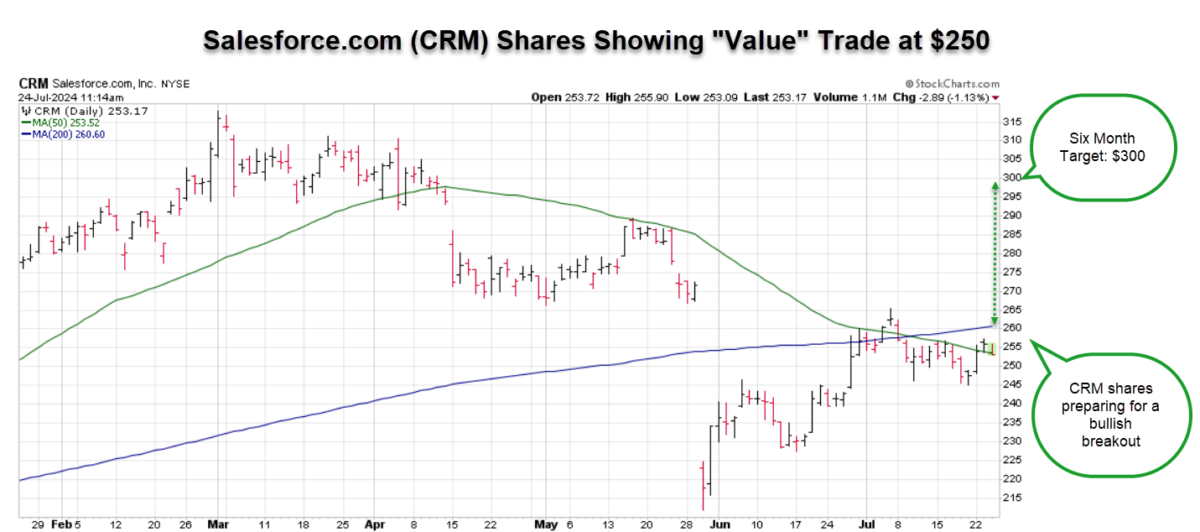

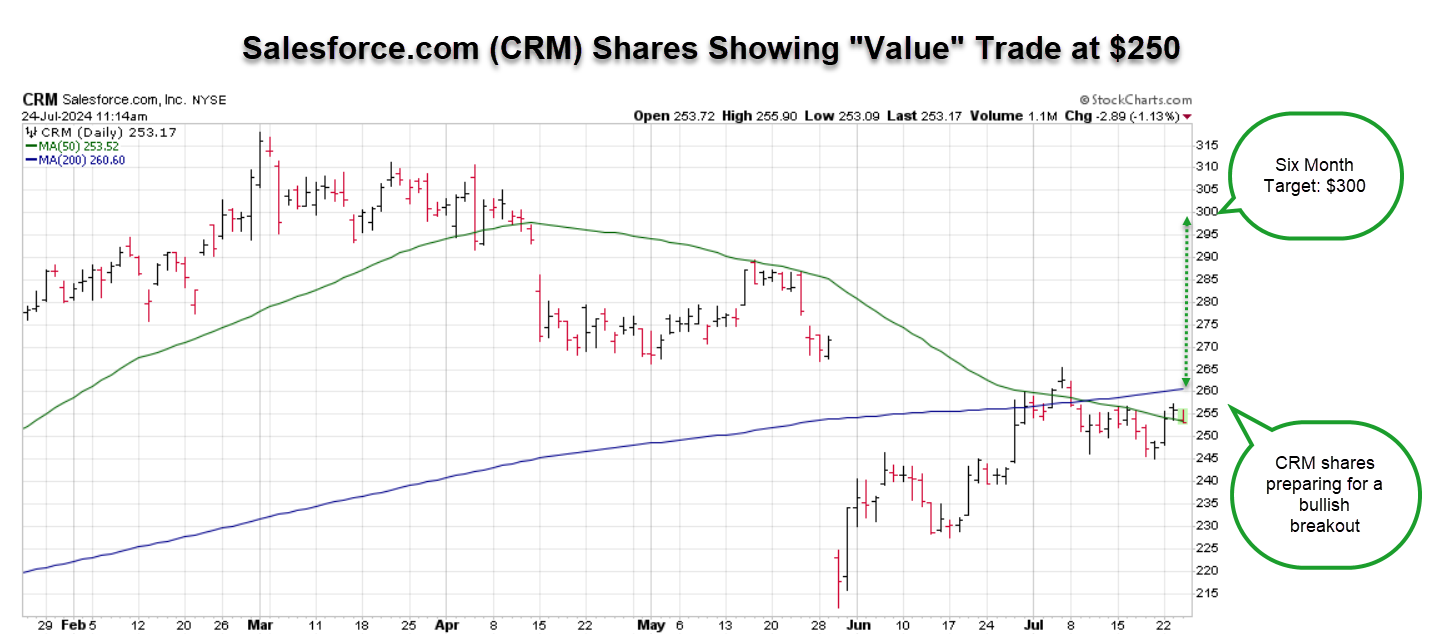

Salesforce.com’s chart, while ugly over the last three months, indicates that the stock is still in a long-term bull market trend.

The stock’s 20-month moving average currently resides at $225 and trending higher.

From a shorter-term perspective, Salesforce.com is preparing to break back above its 200-day moving average. That move will start to attract technical buyers ahead of the company’s earnings report scheduled for August 21.

Keep in mind that the market is set for some rough trading in the month of August due to seasonal trends. Salesforce.com shares should find initial support at $250, but a market pullback may offer the opportunity to buy shares at a “bargain basement” price of $225.

Watch for the next quarter’s earnings to provide a catalyst for CRM shares to move back above the $250 price with a target of $300.

Gretzky would be proud!